Apple Card Review (2024.10 Update: $75 Offer)

2024.10 Update: The $100 offer is expired.The $75 offer is still alive.

2024.8 Update: There’s $100 offer now.

2024.1 Update: The $75 offer is expired.There’s no welcome offer now.

Application Link

Features

- $75 offer: earn $75 after making one purchase in the first 30 days.The recent best offer is $100.

- Earn 3% cashback on Apple, 3% cashback on selected merchants via Apple Pay, earn 2% cashback everywhere via Apple Pay, and earn 1% cashback everywhere else.

The list of 3% merchants are:

- Exxon/Mobil

- Uber & UberEATS

- Walgreen’s

- Duane Reade

- Nike

- T-Mobile store

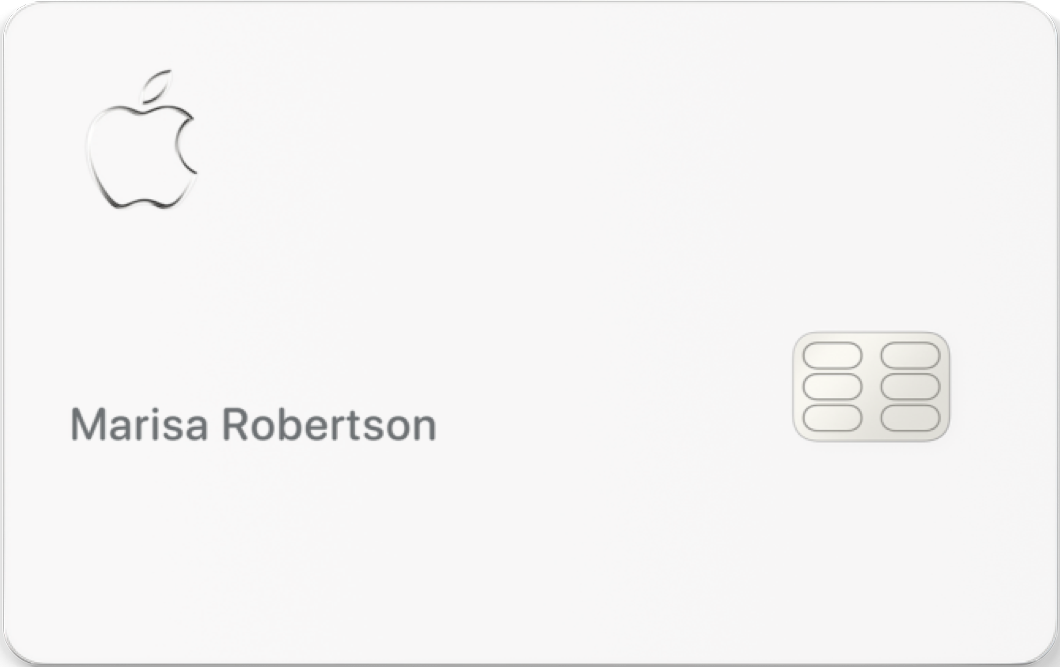

- Apply on iOS devices for the card.After that, you can request a physical card.The physical card is made by Titanium.There is no card number, no CVV, no expiration date, no signature on the physical card.

If you need a card number, you can get a virtual number in the Wallet app on iOS devices.

- You only enter the last 4 digits of your SSN when you apply.Goldman Sachs is the card issuer and will give you a decision about credit limit and APR first, and then let you decide whether to continue.If you choose not to continue or get denied, there will be no hard pull (HP).There will be HP only after you continue and finish the whole process.

- No foreign transaction fee.

- No annual fee.

Disadvantages

- Sign-up bonus is low.

Summary

This is an attempt to challenge the current credit card market by Apple.

It has deep integration with iOS devices.Compared to the earning structure of this card versus other cards, it is OK but not great.You can get 2% cashback in most places via Apple Pay.For the people who want to maximize credit card rewards, this card is not for you.

But the card looks fancy, and maybe the Apple logo is a sufficient reason for some people to have it.

Historical Offers Chart

Application Link

If you like this post, don't forget to give it a 5 star rating!

[Total: 8 Average: 4.5/5]

Disclaimer: This story is auto-aggregated by a computer program and has not been created or edited by mycardopinions.

Publisher: Source link

Publisher: Source link

Leave a Reply

Frequently Asked Questions

Certainly. Unlike personal loans, you won't face any penalties for settling your balance ahead of schedule. However, it's crucial to keep in mind that if your credit card comes with a 0% introductory offer, it's essential to clear your balance completely before the 0% promotion expires and interest charges apply.

However, you can include additional cardholders, each with their own card. While sharing the single credit limit, the primary cardholder remains responsible for settling the debt.

Potentially, yes. Credit card APRs are typically variable, allowing lenders to change rates, impacting your monthly payments. Additionally, be mindful that introductory 0% offers can lead to higher interest rates once they expire. So, it's wise to clear your balance before that happens, if feasible.

Indeed, credit builder cards exist for those with less-than-ideal credit scores. These cards offer lower credit limits (typically £150 to £1,200) and higher interest rates. Responsible use, including full and on-time payments, can gradually boost your creditworthiness, potentially opening doors to better credit card offers down the line.